Main Takeaways

- The 2025 outlook for the beef cattle sector is positive with low supplies meeting high demand to create elevated prices.

- In the near term, the higher risk appears to be beef demand—because of likely high beef prices and ample animal protein competition in the year ahead.

- Herd rebuilding indicators should be watched carefully as the cattle cycle may be approaching its next low in 2025.

The upcoming year is forecast to be another good year for the beef cattle sector in Georgia. Beef demand remains strong despite high prices, and cattle supplies appear to be limited in the year ahead. This combination will likely lead to high prices for beef cattle in 2025. Risks to this outlook come from demand weakness or indications that cattle supplies are increasing in the near term, both of which appear to be relatively low probability at this time.

2024 in Review

In 2024, despite significantly fewer cattle, beef production edged higher year over year. The USDA estimates that beef production in 2024 increased by 0.2%. Higher cattle weights drove this increase. Commercial cattle slaughter in 2024 (through October) was approximately 3% below the levels of the same time period in 2023. Average cattle dressed weights through October were up a remarkable 3.3% in 2024 compared to 2023. Lower cattle slaughter numbers came mostly from lower cow slaughter. Commercial cow slaughter was down nearly 15% through October. Because of lower slaughter, imports of beef jumped significantly year over year. The USDA estimates that total beef imports increased by more than 20% in 2024 to over 4 billion pounds.

Amid high beef prices, demand was very strong in 2024. The USDA estimates that beef consumption in the U.S. increased to 59.5 lb per person in 2024 (up 2% from 2023). This would be the highest since 2010, and comes despite beef prices being consistently higher year over year. Export demand also was strong outside the U.S. While total tons exported dropped through October, total value exported increased.

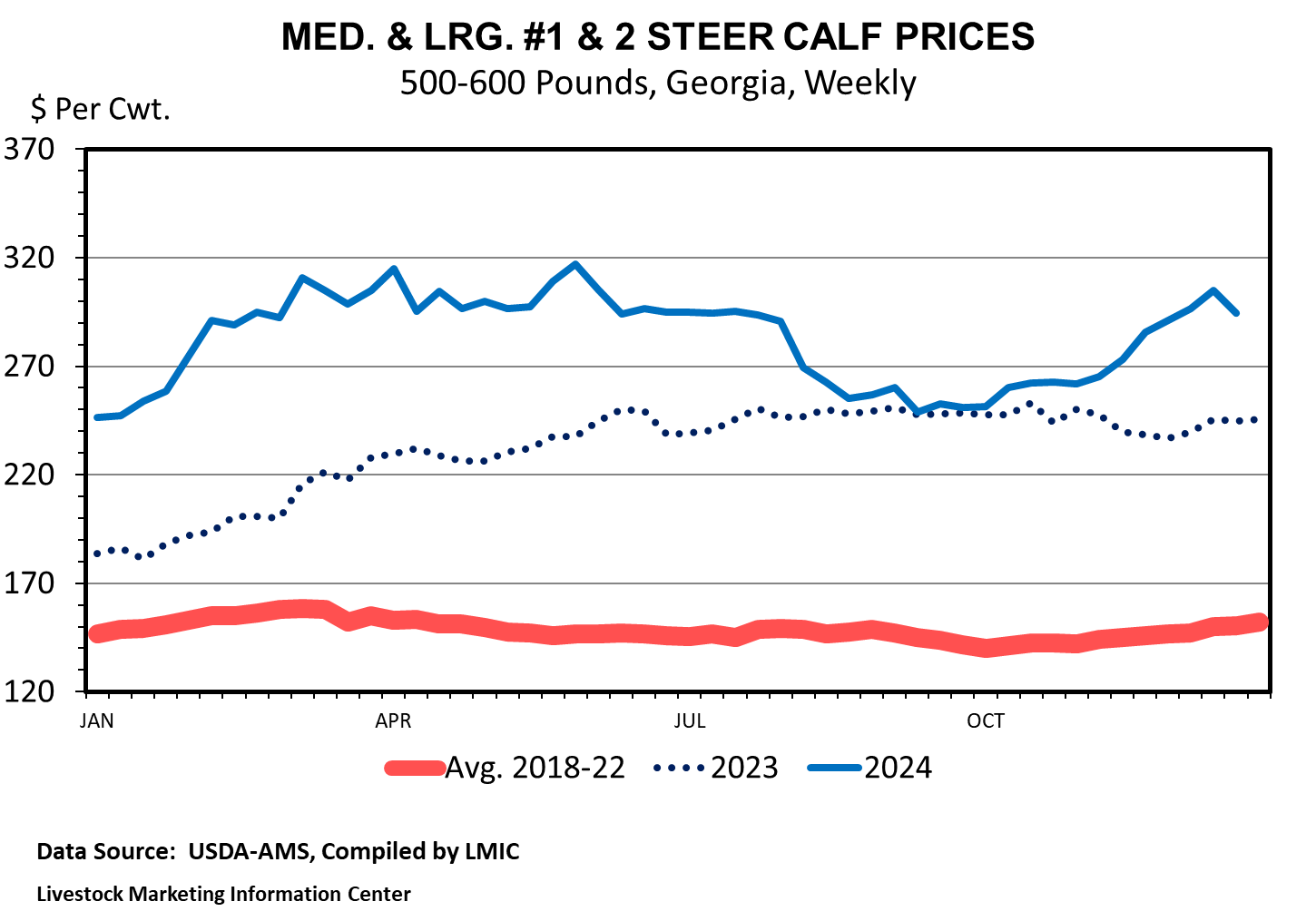

This strong consumer demand filtered back through the supply chain to beef cattle producers. Feeder cattle prices were elevated compared to last year for much of the year. However, prices slid in early fall to similar levels to last year for many areas of the country. In Georgia, feeder cattle prices followed a similar pattern (Figure 1). Medium and large steer calf prices averaged $258.65/cwt in January, 40% higher than in January 2023. In May, average prices were $304.07/cwt (up approximately 30%). In October, prices moderated in line with seasonal patterns to $259.69/cwt (up just 5%). In the fall, heavier-weight steers and heifers saw prices a little lower compared to 2023.

Figure 1. Weekly Georgia Calf Prices, 500–600 lb Steers.

Georgia's basis (i.e., Georgia cash prices minus futures prices) was also very high compared to last year and the 5-year average for lighter-weight calves. For example, from January to July, the average basis in Georgia for 500–600-lb steers was nearly $40/cwt higher than normal. Basis strength for heifers and for heavier-weight steers was smaller to negligible compared to historical averages, respectively.

2025 Outlook

The outlook for the year ahead is positive. Markets are currently pointing to another high-priced year. Futures prices are higher for feeder cattle through next year. Combined with strong basis, indications are that beef cattle producers in Georgia could see similar or higher prices in 2025.

Fundamentally, cattle supplies are likely to be lower in 2025 compared to 2024. With cheap feed and high fed-cattle prices continuing in 2025, high carcass weights will be another story in the year ahead. This will only partially help offset lower cattle supplies.

Much of the industry discussion is on herd rebuilding. All signals in 2024 indicated that the industry continued contracting. Cow slaughter in 2024 was still slightly higher than what previous rebuilding periods would suggest. Additionally, heifers as a percent of cattle-on-feed remained elevated.

In 2025, the industry may be approaching the low in cattle inventory numbers and starting to rebuild. Cow slaughter very well could dip to a point that indicates the herd is rebuilding in the year ahead. Additionally, estimated margins have been very strong for a few years and are projected to remain strong for the near future. Lastly, feed is relatively cheap, and forage is relatively abundant for much of the country. Any rebuild likely will be slower than the most recent expansion phase because of higher interest rates and the smaller base that the cattle herd is rebuilding from.

The more significant short-term risk to the outlook is from demand. With projected smaller beef production and higher cattle prices, beef prices likely will move higher, testing U.S. consumers’ ability and/or willingness to pay for beef. Additionally, any macroeconomic headwinds (e.g., global economic slowdowns or rising unemployment in the U.S.), could affect consumer demand with less-expensive animal protein alternatives readily available.

Source : uga.edu