By Kenny Burdine

While spring is typically the high point for calf prices, 2022 marks the third straight year that something significant has taken some steam out of the markets. A global pandemic hammered feeder cattle prices in 2020 and kept our calf market from reaching the levels that were expected. Some of that also spilled into 2021 and was combined with sharply higher grain prices. As we move into spring of 2022, we have the implications from the war in Ukraine, which is impacting the market in many ways.

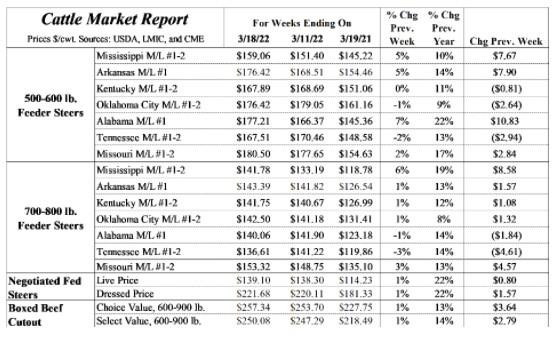

James did a great job walking through these implications on the cattle markets in last week’s article. Rising feed costs, domestic demand concerns from higher fuel prices, increased transportation costs, and several other factors are impacting cattle prices as you read this. The markets have been attempting to price in these uncertainties for the last few weeks, which has led to a lot of volatility. Markets were generally improved last week, as can be seen in the table below. But, volatility is likely to stay with us as things continue to evolve and the market processes what those changes mean for cattle values.

In the spring, calf markets are primarily driven by fall feeder cattle futures and are partially insulated from feed price impacts because many calves are placed into grazing programs. As I write this on March 21st, fall feeder cattle futures are off $3-5 per cwt from mid-February. While that definitely impacts their value this spring, it is not enough to offset the seasonal improvement that is typically seen this time of year. Rather, it just limits how much the calf market can run. Unlike calves, grass doesn’t buffer the feed price impacts on heavy feeders as they will be placed on full feed when sold. Additionally, they will be harvested in the fall and deferred live cattle futures have also decreased in recent weeks. So, we have seen more impact on heavy feeder cattle prices than we have on calf prices.

As frustrating as the market situation is, the fundamentals are much better this spring than they were in either of the previous two springs. While price expectations for 2022 have been lowered over the last few weeks, it is worth noting that prices are much higher now than they were in the spring of 2021. The feeder cattle and calf markets that we track are up by 13-14%, on average, from a year ago. Boxed beef prices are up by a similar percentage and fed cattle prices are up by 22% from 2021. This is significant and the fundamental picture is likely to become more bullish throughout the year. Heifer retention was down to start the year, which painted a picture of a decreasing cowherd again in 2022. And, drought conditions continue to persist in much of the country. If that trend continues, it is likely that additional cow culling will become necessary throughout the year.

Source : osu.edu