By Josh Maples

The optimism surrounding cattle markets at the start of this year is the highest since 2014-2015. Cattle supplies tightened in 2022 while beef demand remained relatively steady. We are entering 2023 with the expectation of a smaller calf crop that is more similar in size to 2014 than to recent years. There will be challenges ahead, especially with navigating higher input costs and questions about beef demand in 2023. But the overall projection is for stronger cattle market prices.

2022 was a unique year for cattle production and markets. James reviewed last year in the last newsletter of 2022 (available here). The rate of beef cows and heifers processed was particularly noteworthy. Around 12 percent more beef cows and about 5 percent more heifers were processed in 2022 than in 2021. The resulting impact for 2023 is these cows and heifers will not be producing calves this year. Although it is only January, the stage is already set for tighter cattle and beef production in 2023. Such is the cyclical nature of the cattle industry – production decisions have long impacts.

Cattle markets improved throughout 2022. Fed cattle prices are up nearly $20 per CWT above year-ago levels. Feeder cattle prices are also up. If we compare to two years ago, the differences are stark. Fed cattle prices have improved by $50 per cwt since December 2020 when markets were still wrestling with the worst of the pandemic impacts – approximately a 50 percent increase.

Higher grain prices continue to be a challenge for producers. U.S. Drought conditions worsened near the end of 2022 and how long dry conditions persist into 2023 will be a key driver for cattle markets. Many areas have received rain in recent weeks which helped improve the drought monitor some. High cattle prices could send signals to expand, but producers will still need adequate pasture or economical feedstuffs to do so.

The December 1 Cattle on Feed estimates were released just before Christmas. The report showed cattle on feed at 11.7 million head which was nearly 3 percent lower than December 1, 2021. This was the third consecutive month with a lower than year-ago total. Placements during November were down 2 percent year over year while marketings were up 1 percent. Feedlot supplies typically peak seasonally during the winter, but December was a decline from November in 2022 (see chart above). It will be interesting to see whether the one of the coming months tops the November total or if we have already reached the seasonal peak.

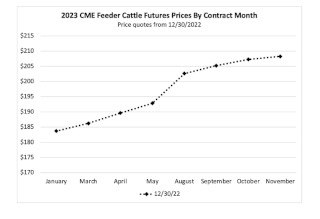

Looking ahead, CME futures prices for 2023 contracts are trading at levels not seen since 2015. All of the fall 2023 feeder cattle contracts are above $200 per CWT and the spring contracts are near $190 (see chart above). The 2023 live cattle contracts are near $160. The start of a new year is a good time to consider price risk management opportunities (click here to read Kenny’s February 2022 newsletter about risk management considerations). The current optimism in markets will very likely allow for stronger pricing opportunities than in past years. Whether you consider using futures, options, or USDA’s Livestock Risk Protection (LRP), there are tools available for producers of every size to offload some price risk if you wish to do so.

Source : osu.edu