By Don Shurley

Eighty cent fever is running rampant. New crop December 17 futures have made a great run and the uptrend is strong. Support seems to be firm. New crop cotton has gained almost a nickel since the first of the year. Currently, old crop May 17 futures are at 77 cents/lb. and this year’s crop, December 17 futures are at 75 cents/lb.

In a meeting earlier this week with a group of cotton producers, I was asked “Where would you be on 2017 crop marketing at this point?” Well, before we get to my answer, let’s first look at the situation.

US cotton acres will increase this year. Anyone who doesn’t know this doesn’t know cotton and/or isn’t paying attention. The National Cotton Council survey estimate was 11 million acres. USDA, at their annual Outlook Forum two weeks ago, pegged acreage at 11.5 million. The USDA-NASS estimate will be out March 31. Regardless of which number you want to go with, US acreage will be up this year, and yet December futures stand at 75 cents with limited weakness below the 70- 72 cent area.

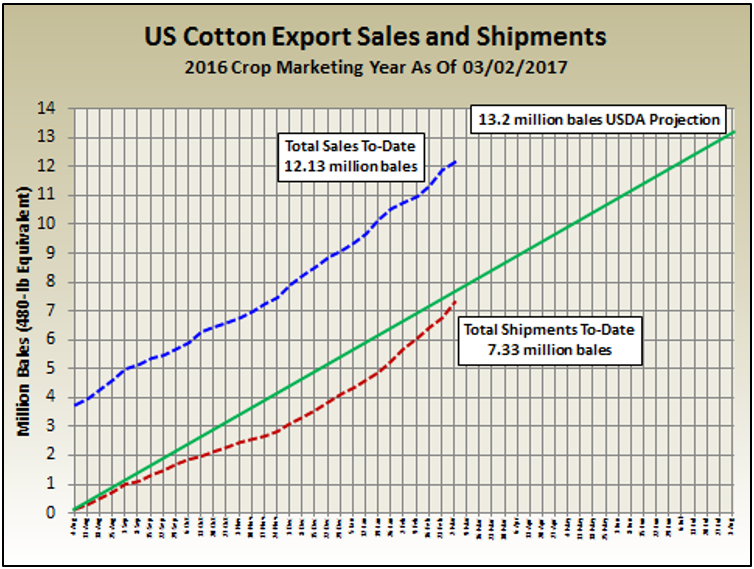

US exports are doing extremely well. In the March USDA estimates that came out yesterday, projected exports for the 2016-17 crop year were raised ½ million bales to 13.2 million. This makes the second consecutive month that exports have been increased—from 12.5 million bales in January to 12.7 in February and now 13.2 in March.

Exports are significant in the outlook for things to come. Look, China—historically our largest customer, is limiting imports for the second consecutive year, and yet we are still projected to export 13.2 million bales. If realized, this would be the highest exports since the 2010 crop year, and achieved without China being a big buyer.

To-date (as of the latest report), export sales total 12.13 million bales—92% of the USDA estimate. Actual shipments have thus far totaled 7.33 million bales—56% of the USDA estimate. Shipments lagged behind pace for a while but have picked up.

The largest customers for US cotton have been mills in Vietnam, China, Turkey, Indonesia, and Mexico. Sales to China have been 1.88 million bales—only 15% of our total sales, but more importantly, this is more than double what was sold to China for all of the last marketing season.

World stocks are declining. Stocks are still high by historical standards, but this is irrelevant. The market knows most of these stocks (that are in China, by the way) are not going anywhere for the time being. So, it’s like they’re not even there.

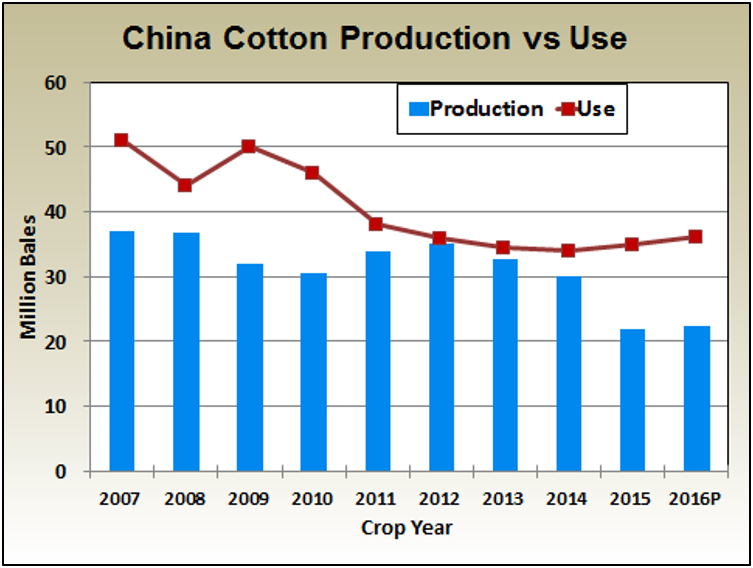

China has curtailed cotton area and production and limited imports and will attempt to utilize its stocks instead. There is a large gap between China’s production and mill use—providing opportunity to use stocks or import if needed/desired.

China sold off over 12 million bales of its stocks during 2016, and another round of sales began this week. All eyes will be on these sales—how are sales doing compared to last year? What is the quality and price?

Last year, the availability of these stocks seemed to provide a little boost to China’s mill industry. After years of decline in the demand/Use of cotton, Use has begun to slowly recover.

The demand or “Use” of cotton still has a long way to go. World Use for the 2016-17 crop year is projected to be 112.43 million bales—down slightly from the February estimate, and 1% higher than 2 years ago, and last year. Although demand/Use is not growing, US market share of exports has increased.

Early 2017 Outlook

December futures are currently in the 75-cent area. No one knows where prices will go. I can draw you up a scenario for 80-cent cotton, and also one for 65-cent cotton, and either one could be equally likely to happen.

I’ve outlined 4 “factors” in play. More than anything else, the good prices we’re seeing at present for 2017 are riding the coattails of the 2016 crop—demand is at least stabilizing, stocks are on the decline, and US exports are going like gangbusters.

The market knows full well that US acreage will be up this year. Prices have not yet reacted to that because:

- Acres actually harvested and yield are what really counts.

- What if exports continue to do well for the 2017 crop?

- What if the China “gap” gets wider?

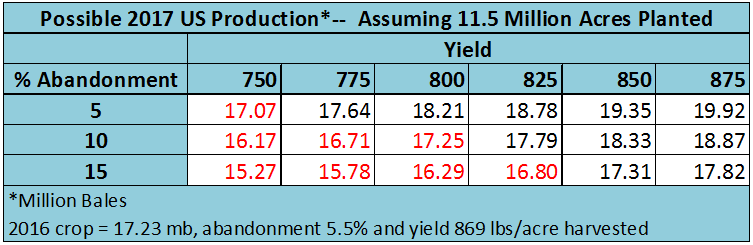

The 2016 crop is currently estimated at 17.23 million bales. Acreage abandonment has been low for 2 consecutive years—5½% for the 2016 crop, and 6% for 2015. Assuming 11.5 million acres are planted (14% more than last year), the US crop could be equal to or less than last year, if abandonment is more normal—depending on yield.

Is it likely that 2017 crop prices could eventually come under pressure, if the expected crop is large, due to even more acres planted or good progress and conditions. Of course, this could be offset by continued strength in exports and US market share.

With new crop December futures in the 75-cent area, I know producers are considering taking protection. Some already have even when prices were 72 to 73 cents/lb.

Although basis obviously varies and has weakened recently, here in the Southeast the basis for 41-4/34 has averaged about even the futures, and premiums for 31-3/35 or better have been around 200 to 250 points.

Forward (fixed price) bale contracts at an even or better basis the December futures provide a good opportunity. One concern, however, might be whether or not the contract will pay premiums for Color and Staple. If not, producers could see this as a deterrent, unless the basis is very good.

If you want to take protection but retain the opportunity to do better if prices were to increase, you can do that with a minimum price contract or a Put Option. On a minimum price contract, typically the basis is not going to be as good and with a Put, you have to pay the premium. But in both cases, you could benefit if prices go up. With a Put, you could possibly recoup the cost of the premium by being able to sell your cotton on the spot market and capture quality premiums not offered on a contract.

OK, I was asked where I would be on 2017 pricing. I tend to be fairly conservative and cautious in my outlook. For 2017, I want some 80-cent cotton if it gets there, but I don’t want to be stuck with the majority of my crop to sell if the market dips to 68 or below. Right now, I believe I would be 1/3 in at this point.

Source:ufl.edu