By Derrell S. Peel

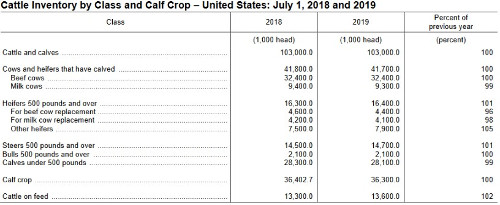

USDA’s July Cattle Report shows that the inventory of all cattle and calves in the U.S. was unchanged year over year at 103 million head as of July 1. The inventory of beef cows was likewise unchanged at 32.4 million head, while the dairy cow inventory was down 9.3 million, -1.1 percent year over year. Beef replacement heifers were down 4.3 percent at 4.4 million head, and dairy replacement heifers were down 2.4 percent to 4.1 million head compared to one year ago. The inventory of bulls was unchanged year over year at 2.1 million head.

The July 2019 Cattle Report shows that inventory totals for the U.S. cattle herd has reached a plateau. Source:

Cattle (July 2019) USDA, National Agricultural Statistics Service

The July 1 inventory of steers over 500 pounds was 14.7 million head, up 1.4 percent year over year. The inventory of other (not for replacement) heifers over 500 pounds was 7.9 million head, up 5.3 percent from one year ago. Total steer and heifer calves under 500 pounds was 28.1 million head, down 0.7 percent year over year. With an estimated total July 1 feedlot inventory of 13.6 million head, these inventory estimates lead to an estimated feeder supply outside of feedlots of 37.1 million head, up slightly by 0.3 percent compared to last year. The inventory report was well anticipated and contained no surprises.

These inventory totals suggest that the U.S. cattle herd has reached a plateau. I contrast a plateau with a more typical cyclical peak inventory that historically has implied a liquidation phase to follow. The current inventory levels do not suggest a need for, or an inevitable, liquidation in cattle inventories at this time. Stable cow numbers and calf crop suggest that beef production will show little or no growth going into 2020. Current beef production levels and cattle prices are sustainable until something changes to provoke a new direction in cattle inventories.

Such changes could come sooner or later and could be positive or negative. If both domestic and international demand for U.S. beef continues at current levels, there will be little or no pressure on cattle markets. If something should happen to weaken beef demand in the U.S. or in global markets, lower beef and cattle prices could result in some liquidation of cattle inventories. Impressive beef demand since 2017 is showing some signs of weakness that should be closely monitored going forward. Conversely, new growth in demand, most likely to occur if the myriad of trade disputes and issues in which the U.S. is currently embroiled are resolved, could provoke additional herd expansion and new growth in beef and cattle markets at some point.

The U.S. cattle and beef industry may be in the most stable situation that I can ever remember. This is pretty remarkable given the continued turbulence in external market conditions. Numerous factors that could destabilize cattle markets should be monitored including; corn prices and feed market conditions; the impacts of African Swine Fever on global protein markets; U.S. macroeconomic conditions; and exchange rates among others. Additionally, progress or lack thereof on current trade politics or new trade issues that could arise will have a large impact, positive or negative, on the overall climate for beef and cattle markets.