By James Mitchell

In my last article, I reviewed some basics of Pasture, Rangeland, and Forage Insurance (PRF). I noted that there are several decisions that producers will have to make about their PRF policy. Those decisions have important implications for producer premiums and indemnity payments. This week I want to continue that discussion by looking at some of these PRF decisions that interested producers will have to consider. To do this, I will utilize the USDA RMA decision support tool and our example from last time, the UofA Livestock and Forestry Research Station in Batesville, AR.

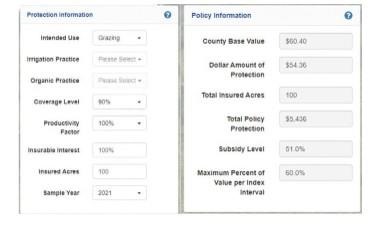

An example of the PRF protection decisions that a producer will make.

The figure above is an example of the PRF protection decisions that a producer will have to make. These PRF decisions included intended use, insured acres, coverage level, productivity factor, two-month index intervals, and percent of value. There are two approaches that producers can take with these decisions. The first is to approach PRF from a risk management perspective. The second is to make PRF decisions that maximize the likelihood and amount of indemnity payments. These perspectives do not always agree with each other.

Intended Use:

Producers choose the intended use of the insured forage acreage. The options are grazing and hay. Grazing acreage has lower per acre premiums and lower per acre indemnity payments when a loss is triggered. Obviously, producers should choose the intended use that matches the primary use of the forage. In our example, we have selected grazing as the intended use of our forage acreage.

Insured Acres:

Producers choose how many acres to insure for a PRF policy. Unlike other crop insurance products, producers do not have to cover all of their forage acreage though that is an option. Producers using PRF for the first time might find it beneficial only to insure part of their pasture or hay acreage. In our example, we are insuring 100 acres of pasture.

Coverage Level:

PRF coverage levels range from 70% to 90% in 5% increments. Higher coverage levels are more likely to trigger an indemnity but are also more expensive. Premium subsidy rates will also depend on the chosen coverage level. Subsidy rates range from 51% to 59%. Lower coverage levels have higher subsidy rates. Our example uses the highest coverage level of 90%.

Productivity Factor:

USDA-RMA calculates a county base value of production. The productivity value allows the producer to adjust how much of the base value to cover. The productivity factor ranges from 60% to 150%, and relative to the RMA base value changes how much coverage to buy. Producers with high-quality pastureland might choose a productivity factor exceeding 100% as the value of that forage is higher, thus requiring a higher dollar amount of coverage. Higher productivity factors are more expensive and have higher indemnity payments when a loss is triggered.

Two-Month Index Intervals and Percent of Value:

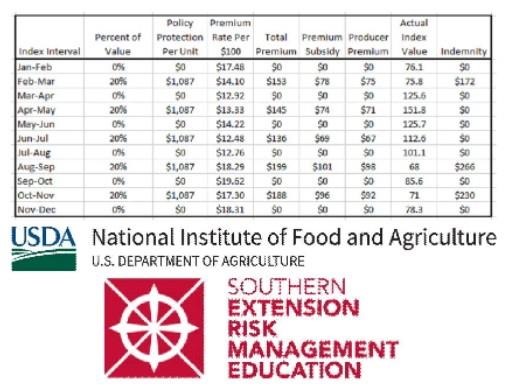

Based on our example, our PRF policy is $5,436 of protection. The final decision is how to allocate the $5,436 of protection across the different index intervals. At a minimum, we must choose two 2-month intervals and cannot exceed six 2-month intervals. For the chosen intervals, we select the percent of value to protect, i.e., the percent of $5,436 to insure in each interval. The table below is an example of allocating the percent of value evenly across five non-overlapping intervals.

Based on the table, our PRF protection totaled $54.36/acre. This policy cost $4.03/acre. At the end of the policy, based on actual index values, indemnity payments totaled $6.67/acre.

This material is based upon work supported by USDA/NIFA under Award Number 2021-70027-34722.

Source : osu.edu