By Gary Schnitkey and Krista Swanson

Market Facilitation Program (MFP) payments have served as a significant source of revenue on grain farms in 2018 and 2019. Without MFP payments, average farmer returns would be negative in 2019, and far below any level since consistent records began in 2000. Without MFP payments, 2020 returns are projected to be negative. It is unknown at this time if MFP payments will occur in 2020, or the potential level of an MFP payment if the program continues. When developing cash rental rates, we suggest lowering cash rent levels if they are at or above averages for a productivity level, and then having the possibility of higher cash rents if MFP payments occur.

Historic Returns to Central Illinois

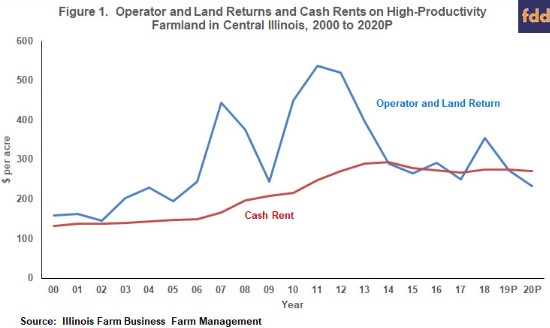

Figure 1 shows average operator and land return and average cash rent on high-productivity farmland in central Illinois, with historical values representing actual returns from grain farms enrolled in Illinois Farm Business Farm Management (FBFM). Documentation for values shown in Figure 1 is provided in Revenue and Costs for Illinois Grain Crops (click here for download). Historical and projected revenue assumptions also are given in a November 19, 2019 farmdoc daily article. Figure 1 shows returns for farmland given that 50% of the acres are in corn and 50% are in soybeans.

Two lines are shown in Figure 1. The first is operator and land return, representing a return to both the farmer and land owner. Costs for farmland are not included in operator and land return. If farmland is cash rented, the cost to the farmer is cash rent. Figure 1 also shows average cash rent in central Illinois. When operator and land return is above cash rent, a farmer will have a positive cash return on cash rented land. Losses occur when operator and land return is below cash rent.

Between 2006 and 2013, a period in which corn and soybean prices were relatively high, operator and land returns exceeded cash rents by large margins. This period was characterized by higher net incomes (see farmdoc daily, November 19, 2019). Cash rents were rising during this period in response to higher operator and land returns.

Average operator and land returns have been roughly the same as average cash rents since 2013:

- 2014: Operator and land return was $290 per acre, cash rent was $293 per acre, and farmer return was -$3 per acre.

- 2015: Operator and land return was $265 per acre, cash rent was $278 per acre, and farmer return was -$13 per acre.

- 2016: Operator and land return was $291 per acre, cash rent was $273 per acre, and farmer return was $18 per acre.

- 2017: Operator and land return was $250 per acre, cash rent was $267 per acre, and farmer return was -$17 per acre.

- 2018: Operator and land return was $355 per acre, cash rent was $274 per acre, and farmer return was $81 per acre.

- 2019 Projections are for an operator and land return of $273 per acre, cash rent of $274 per acre, and farmer return of -$1 per acre.

Lower returns after 2013 largely occurred because of declines in commodity prices. Returns shown in Figure 1 suggest that cash rents should decline because farmers need to obtain a positive return for the risks, labor, and management of farming. Likely reasons that cash rents farmers are paying have not declined are 1) financial reserves built during the period of high incomes from 2006 to 2012 are allowing farmers to continue paying high rental rates in hopes that higher commodity prices in the future will make those rates profitable (farmdoc daily, October 4, 2016 and October 23, 2018), and 2) positive returns from owned and share rented farmland are used to subsidize cash rent farmland (farmdoc daily, August 22, 2017). Trade disputes, and other factors such as African Swine Fever in China, have considerably diminished chances of higher prices in the near future.

Impacts of MFP payments

In 2018, trade disputes between the U.S. and other countries began impacting agriculture, with the tariff battle between China and the U.S. receiving a great deal of attention. Soybean prices declined throughout the year as the trade dispute continued. On central Illinois farms, prices averaged $8.85 per bushel for soybeans produced in 2018, down from the $9.81 average from 2013-2018.

Although soybean prices were down, returns were positive for central Illinois farmers, at the highest level since 2013 (see Figure 1). In 2018, operator and land return exceed cash rent by $81 per acre. Both exceptionally high yields and MFP payments contributed to this higher return. In 2018, MFP payments accounted for $62 per acre of return, with most of that coming from soybean acres (see farmdoc daily, November 19, 2019). Without the MFP payments, farmer return in 2018 would have been $19 per acre, in the range of returns in other years since 2013.

In 2019, farmer return is projected at -$1 per acre. Returns are down in 2019 because of much lower yields. MFP payments have a large, positive impact on returns. For 2019, MFP payments for central Illinois grain farms are estimated at $82 per acre, up by $20 from average 2018 levels (see farmdoc daily July 30, 2019 for a list of payments by county). This $82 level assumes that all three tranches of MFP payments are paid. Two tranches totaling three quarters of the payment amount have been paid. The third tranche, if confirmed, would be distributed in early 2020 with the remaining quarter of the payment. Without a MFP payment, 2019 returns are estimated at -$83 per acre, the lowest farmer return since 2000 (see Figure 1).

Figure 1 also includes projections for 2020. Operator and land return is projected at $232 per acre, cash rent at $270 per acre, and farmer return at -$38 per acre. The 2020 projection is based on a return to trend yields. Exceptional yields like those in 2018 would be needed to get positive returns given prices of $3.90 per bushel for corn and $9.00 for soybeans. However, prices may fall to lower levels if exceptional yields occur. As a result, crop revenue increases alone likely will not lead to higher farmer returns. Positive returns in 2020 may be dependent on some level of support, such as the continuation of the MFP.

MFP Payments in Perspective

In the last two years, MFP payments have been a significant source of revenue on Illinois grain farms. In 2018, MFP payments represented 8 percent of total gross revenue received from corn and soybeans production. In 2019, MFP’s share is presented at 11 percent (see Figure 2).

Government payments have not accounted for that large of a share of gross revenue on Illinois grain farms since the early 2000s. In the early 2000s, government support to farmers through the Agricultural Market Transition Act, Market Loss Adjustment, and marketing loan programs represented a higher share of gross revenue. For example, government payments were 25% of gross revenue in 2000, 23 percent in 2001 (see Figure 2)

Cash Rents

Corn and soybean prices fell and were at lower levels in both the early 2000s (beginning in 1998) and since 2018. Those lower prices then led to governments payments. In the early 2000s, those payments were legislated through Congress. The MFP payments come through different authority, with levels determined through a process that is not transparent (see farmdoc daily, November 21, 2019 for more discussion of the MFP program). Also, the levels of MFP payments from one year to the next are not known. For 2019, administrative officials indicated that MFP payments would not occur up to May 2019. In actuality, MFP payments on most farms will be higher in 2019 than in 2018.

Counterfactuals are difficult to prove, but it seems likely that farmers in the early 2000s would have had to make larger adjustments in response to lower commodity prices had government support not existed. In the end, land returns likely would have declined, and cash rents fallen.

Similarly, cash rents likely would have fallen in 2019 as a result of lower commodity prices in 2018 had MFP payments not existed. The extent to which they would have fallen depends on how participants view the permanence of lower soybean prices. If soybean prices will continue below $9.00 for several years, cash rents need to adjust downward if MFP payments do not continue.

2020 Cash Rents

The uncertainty of MFP payments presents an issue for setting 2020 cash rents. If MFP payments do not occur, farmers could face large losses if cash rents levels are set as if MFP payments will occur. On the other hand, MFP payments at the 2018 and 2019 levels could result in good farmer returns, particularly if yields are exceptional. This uncertainty obviously adds to the difficulty in making cash rent decisions for 2020.

As farmers and landowners negotiate rental rates for 2020, several factors should be considered. Cash rental rates have remained relatively flat despite a lower price environment since 2013. The average central Illinois cash rental rate has put farmer returns below break-even in three of the last five years, and likely right at break-even in 2019 including the full MFP payment.

Given the uncertainty about MFP payment, an appropriate approach would be to set a cash rent without the MFP considered in budgeting and allowing for an increase in the rent if the MFP occurs. As an example, consider 2020 projections. Without an MFP payment, 2020 operator and land return is projected at $232 per acre. This $232 per acre is considerably below the 2018 average rent of $273 per acre. Setting a cash rent at $230 per acre would result in a $2 projected return to the farmer, not a desirable return, but better than a loss that would result with a cash rent at the $273 average for 2019. The lease could then have a clause that shares the MFP payments 50-50 between the land owner and farmer. If an $82 per acre MFP payment is received — equivalent to the average projected payment for 2019 — the farmer would make an additional payment of $41 to the land owner, resulting in total rent to the land owner of $271 per acre ($230 base cash rent plus $41 payments from the MFP payment), and a $43 return to the farmer ($2 projected return with MFP pulse $41 from MFP).

Several notes about the above lease:

- A share-rent arrangement has risk sharing directly built into the lease. As a result, MFP payments already are considered in share-rent arrangements

- The above lease is very close to a variable cash lease (see farmdoc daily, September 9, 2015 for a discussion of one-type of variable cash leases. Click here for a lease). Variable cash leases would consider possible higher returns due to higher prices or yields. Inclusion of MFP like payments in variable cash leases seems warranted if base levels are low enough such that farmers do not take large losses at base rent levels.

- Base levels need to be set low enough so that farmer risks are reduced. Putting a clause for MFP sharing without lowering cash rents simply shifts returns from farmers to land owners, and adds risk to the farmer.

- The 50-50 sharing percent is dependent on having the base level low enough that farmer risks are reduced. Given the current economic environment, base rent levels should be well below cash rent levels. A method for determining average cash rents for different cash rent levels is presented in a November 7, 2017 farmdoc daily article.

Summary

MFP payments have had impacts on land rental rates. Moreover, uncertainty about the continuation of MFP in 2020 presents issues in setting cash rental rates. Given this uncertainty, we present the idea of setting cash rents at appropriate levels given the price and yield environment, likely lower than 2019 cash rent rates, with contingencies for cases in which MFP payments occur. By doing this, base cash rent is set at a level that allows the farmer to generate profits and leaves open the option for both parties to benefit if MFP payments occur in 2020.

Source : illinois.edu