By James Mitchell

I want to start this article by recognizing that what is happening in Ukraine is a humanitarian crisis. I do not want to overlook those important aspects of the war in Ukraine. That said, I am not a geopolitical expert or war strategist. Many well-informed individuals can offer you a better perspective on those issues.

In this article, I want to discuss the far-reaching implications of the Ukraine war for cattle markets. Inflation, grain markets, and energy markets are the main focus. Fertilizer is another big one. There are also domestic beef demand concerns that we need to discuss. Cattle markets are reacting to all of these.

Perhaps the most noticeable impact of the conflict in Ukraine, at least initially, is market volatility. Uncertainty equals price volatility. The war in Ukraine presents markets with a significant degree of uncertainty. As new information arrives, markets incorporate it into prices. What we know today is different from what we will know tomorrow, next week, next month, etc. Markets are trying to work through that information. Evidence that markets are working.

Volatility makes it harder to manage price risk. I have been asked several times about what producers should do to manage the price swings that we are currently observing. Scenarios like this one are why we use price risk management tools. This is similar to considering price risk management during March 2020. To be blunt, it is hard to manage price risk when you are in the middle of a high price risk situation. There are still things we can do to manage elevated price risk. The best advice is to be as flexible as your operation will allow. Put pen to paper and work through several scenarios.

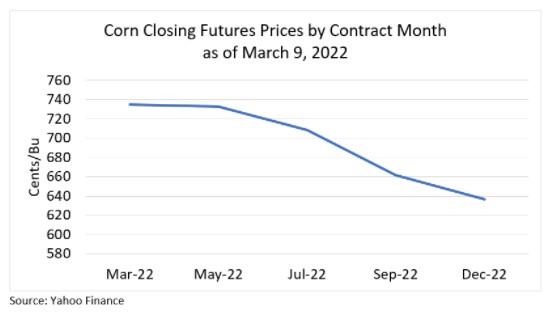

The immediate impact for grain markets is on old crop cash and futures prices. Looking at CME corn futures prices from March 9, the March 2022 corn contract is trading at close to $1/bu over the December 2022 contract. Today’s corn market is an inverted market. An inverted market refers to a scenario where nearby futures contracts are trading at a premium to deferred futures. As my colleague Andy McKenzie likes to say, “an inverted market tells market participants that we want corn now!”

There are also long-term concerns for grain markets. Specifically, will farmers in Ukraine be able to plant? Even if Ukraine can plant a new corn and wheat crop, will they be able to export? There is potential that the current conflict will damage Ukraine’s infrastructure, creating further logistical challenges for grain exporters.

In 2021, Russia was the largest net exporter of oil and natural gas. Approximately 4% of Russia’s crude oil exports were to the United States. Sanctions on Russian oil and gas and the prospect of a complete ban on Russian oil have sent oil prices surging. Prices from Bloomberg show Brent Crude and WTI Crude trading at $105/barrel and $103/barrel, a modest decline from the prior week. Higher oil and natural gas prices mean higher energy costs. These higher energy costs will span the entire beef supply chain. It takes energy to run a meat processing plant. Transportation costs for wholesale and retail will increase. On-farm fuel costs will also increase.

Higher grain, fuel, energy, and fertilizer prices will impact inflation. Food and energy are the most volatile prices included in the Consumer Price Index (CPI) which is one measure of inflation. Food and energy prices are also the most heavily impacted by the war. So, it should be no surprise that we will continue to observe historically higher inflation. The most recent data shows inflation reaching 7.9% in February. Because food and energy prices are so volatile, a better measure to track the price level in the economy is the CPI less food and energy, which is referred to as core inflation. Core inflation reached 6.4% in February. The degree to which inflation impacts consumer spending will depend on, among other factors, whether the wage growth rate tracks inflation. We know that inflation has outpaced growth in wage rates over the past few months. We expect changes in consumer spending.

There are no immediate beef export demand concerns. Russia is largely self-sufficient in meat production. The only concern for U.S. beef exports would be if other countries became directly involved in the conflict. There are domestic meat demand concerns. As has already been mentioned, inflation will impact consumer spending, provided wage growth does not track inflation. Consumers will also experience higher prices at the gas pump. Consumers might be more hesitant to make that last-minute trip to the grocery store. As I’ve said in early articles, beef demand will depend on what retail beef prices do relative to chicken prices, pork prices, and consumer income.

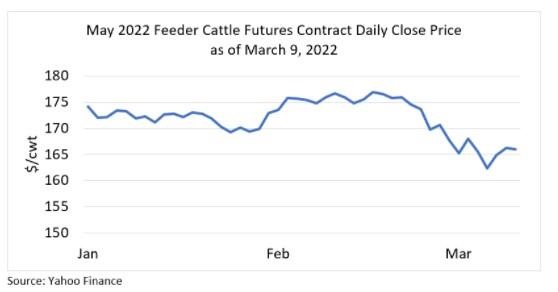

Cattle markets have certainly reacted to the events of the past few weeks. Last Friday, May feeder cattle futures were down 7.5% compared to mid-February. We can all think through the implications for cattle feeding dynamics, hay production, and production costs for cattle producers. Fortunately, the same supportive supply dynamics that analysts have discussed the past few months remain in play. Tight cattle supplies that we expect to get tighter. Yes, this means we have fewer cattle to sell, but it also means higher cattle prices and the potential for improved profitability.

Source : osu.edu