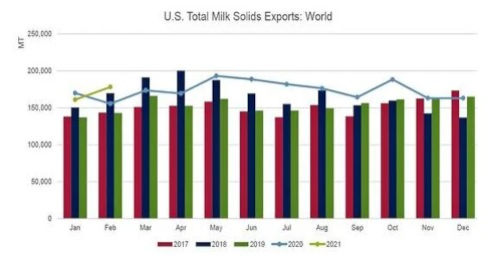

Total dairy export value climbed 7% year-over-year to reach $565.5 million and volume in milk solids equivalent (MSE) jumped 15%. February’s growth was driven primarily by resurgence in nonfat dry milk/skim milk powder (NFDM/SMP) to Mexico and Southeast Asia and whey products to China.

More information, data and charts on specific products and markets can be found here.

Below are our three main stories for the month:

NFDM/SMP exports an uplifting surprise

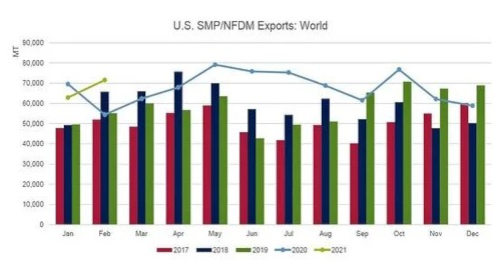

February’s NFDM/SMP export data surprised us. Frequent reports of shipping frustrations delaying exports have been the story for months. Logistics delays drove the declines we saw in U.S. NFDM/SMP exports in November, December and January. And the preliminary data suggested that was going to be the case in February.

USDA’s Dairy Product Report showed growing inventories of NFDM – reaching 156,766 MT in February. That figure was up 18,419 MT from January despite less NFDM/SMP produced. This suggests reduced commercial disappearance. And yet, NFDM/SMP exports grew substantially. Total NFDM/SMP exports grew 31% (+17,120 MT) over February 2020 with volumes gaining to both Southeast Asia (+38%, +8,421 MT) and Mexico (+30%, +5,936 MT).

From this, we can infer a few things:

First, domestic disappearance of NFDM was very weak in the first part of the year. Taken at face value, if production was down and exports were up but inventories still grew, then the culprit must have been reduced domestic disappearance.

Second, we can assume that the February exports were predominantly SMP produced in Q4 of last year that was able to make it onto a boat for export. The growing inventory figure from USDA only tracks NFDM, so to make the math work, the exported product must have been predominantly SMP.

Third, and perhaps most importantly, the surge in exports – particularly to Southeast Asia – suggests that international demand is better than the global trade figures implied over the past several months. Global NFDM/SMP trade declined five months in a row from September 2020 to January 2021, even as prices have steadily climbed. However, combine February’s robust exports, anecdotal reports that the product that is in inventory is sold, and the gain in Tuesday’s GDT, and the picture you get is of strong international demand for SMP, but shipping delays limiting the ability to fully meet that demand.

Looking ahead, this suggests that if U.S. exporters can secure booking with a carrier, there will be opportunities to grow exports.

Cheese volume highest in seven months

The U.S. exported 30,176 MT of cheese in February. It was the first time monthly volume exceeded 30,000 MT since last August – and it was done in a month with only 28 days. Adjusting for Leap Day, February 2021 U.S. cheese exports grew 1.1% over February 2020.

While cheese exports for the first two months still lag January-February 2019 and 2020, there were some optimistic signs in the February numbers.

Looking at individual market performance (NOT adjusted for Leap Day), U.S. suppliers saw broad-based geographical gains in February, led by a 70% increase in sales (+1,062 MT) to the Middle East/North Africa (primarily Saudi Arabia and the United Arab Emirates). Exports were also strong to Japan (+263 MT), China (+201 MT), Oceania (+192 MT), Central America (+189 MT) and South Korea (+188 MT). (U.S. cheese exports to Japan and South Korea in the first two months were up 20% over the same period in 2020.)

That diversified success in February helped mitigate an 11% decline in cheese exports (-1,019 MT) to our No. 1 market, Mexico. It was the United States’ sixth consecutive year-over-year monthly decrease in cheese sales to Mexico, but at 8,591 MT, February was the largest volume since August 2020.

More competitive U.S. cheese pricing since December and progress in keeping COVID-19 in check in key markets in East Asia and the Middle East (and subsequent improved foodservice traffic in those markets) are creating a more optimistic outlook for U.S. cheese. But U.S. shipping issues and continued COVID-19 uncertainty remain strong headwinds to a full cheese rebound.

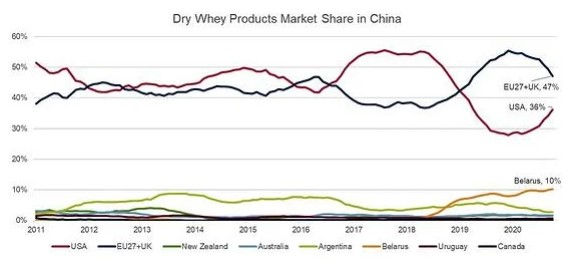

Continued strong whey exports

U.S. whey exports rose 29% (+11,500 MT) in February, continuing the march of strong global whey demand, and it comes as no surprise that China led the way. U.S. whey exports to China in February more than doubled, up 159% (+16,270 MT) compared to February 2020. Year-to-date total U.S. whey exports grew 22% (+17,700 MT) with year-to-date exports to China up 120% (+27,400 MT).

Along with the U.S., the EU is the other major provider of whey products to China; however, the EU product mix is weighted toward more high-value whey products where the U.S. is a primary provider of whey products used in feed in China. China’s continuing efforts to rebuild its swine herd has increased demand for whey in feed and as such has led to increased U.S. whey exports and rising U.S. market share.

Click here to see more...