By Logan Garcia

The following is a recap of fertilizer price trends and market developments for November and the first half of December.

AMMONIA

Domestic: Ammonia prices remained largely steady in the U.S. in November as fall deliveries continued to roll out for application to fields following the completion of most of the corn and soybean harvest in the U.S.

An ammonia distributor in the Corn Belt said they have continued to see strong deliveries after an "extremely fast start to the season." Most of this activity still centers on previously booked tons, however, leaving the spot market flat despite surging applications and ammonia deliveries in the country.

Corn Belt spot values by the end of November were indicated flat from the previous month at $700-$725 per short ton (t) free-on-board (FOB, or sales price without transportation costs included).

Offers from ammonia producers in eastern Oklahoma-area nitrogen plants also saw no new indicated prices on account of spot availability being near nonexistent while producers fulfill previous commitments. At the end of October and into November, price levels in the region were assessed at $680-$700/t ex-works (seller makes a product available at a designated location, and the buyer of the product must cover the transport costs).

Following the latest drop in Tampa ammonia prices in late December, ammonia prices are expected to remain stable to softer as the wider market continues its downward correction.

International: The global ammonia market came under pressure in November due to several factors, including the return of Ma'aden's 1.089-million-metric-ton-per-year ammonia plant in Saudi Arabia to full operation, as well as the consequence of cheaper-origin ammonia sales into Europe and the Mediterranean region.

On the back of these downward corrections in the global market, Yara and Mosaic settled late Wednesday, Nov. 29, at $625 per metric ton (mt) CFR (cost and freight -- the seller pays the costs to export the goods and for the freight) Tampa for December deliveries -- a rollover from the previous settlement for November deliveries at Tampa. This was later considered to be too high, leading to a $100/mt decrease for January shipments.

Similarly in the Black Sea, prices fell approximately $30-$40/mt from October levels to end November at $555-$615/mt FOB. Meanwhile, in northwest Europe, prices consolidated from a wider range of $580-$680/mt CFR duty-paid in October to November's final assessment at $640-$675/mt.

Ammonia price levels were expected to continue decreasing as the market corrects and decides what new prices will be appropriate in the lead-up to 2024.

UREA

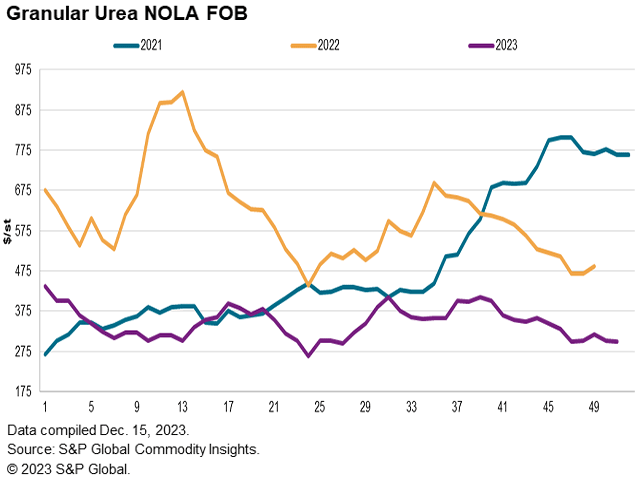

Domestic: Urea prices continued to drift in November following the conclusion of another India tender and limited domestic demand in the U.S. Gulf and upriver terminals.

For this winter so far, and generally typical of the time of year, subdued interest from U.S. buyers for prompt tons led to a slide in domestic price levels as well as dependence on looking abroad toward markets like India for indications on latest market prices.

NOLA (New Orleans, Louisiana) prices ended November lower, with liquidity limited around the Thanksgiving holiday in the U.S. The last Fertecon assessment of November leading up to the holiday was assessed $325-$335/t FOB, lower for the third consecutive week and down compared to $345-$355/t FOB at the end of October.

River terminal offers are said to be slightly lower month-over-month at $455-$470/t FOB ahead of final closures to barges for markets north of St. Louis, down from $465-$475/t FOB in late October.

On lower ammonia prices as well as dipping values in other nitrate fertilizers, urea prices were similarly expected to be softer to stable in the short term.

International: Sluggish demand and ample supply continued to subject global urea markets to significant downward pressure in November. With buyers holding firm in their wait-and-see approach, significant demand was not expected to resume until the new year.

Even though prices in Brazil had a small rebound to $310-$320/mt CFR higher from the end-of-October assessment of $395-$405/mt CFR, the impact of climatic conditions on the market is getting clearer. Data published by Globo Rural showed fertilizer trade volumes in 2024 were set to be lower than in the last four years. Meanwhile, Egyptian sellers achieved price levels to end November at $345-$350/mt FOB, down from sales at $365-$375/mt FOB earlier in the month.

Suppliers are expecting a quiet end to the year, especially following news a fresh Indian tender has been delayed until January. The general price downturn stems more from seasonal than structural aspects, with current crop prices modestly higher yet lagging behind previous years, challenging urea's affordability and value proposition.

UREA AMMONIUM NITRATE (UAN)

The U.S. nitrogen market was mostly steady across November with deliveries for the fall fertilizer application period continuing to move on mostly pre-bought volumes booked over the summer.

Overall, the U.S. UAN markets remained stagnant, although demand appeared set to emerge early in first-quarter 2024. As a result, no change was heard to UAN 32%N barge price indications at NOLA, leading us to carry our October assessment across November at $240-$260/t FOB.

The East Coast market was similarly flat from the last report with the latest indications persisting at $275-$280/mt CFR, unchanged from our assessment at the end of October.

Along the Mississippi River, terminal prices for 32%N UAN were also unchanged with Cincinnati priced around $290/t FOB, slightly higher from other river hub locations such as St. Louis.

Following recent price corrections, UAN is expected to see good demand in spring 2024 with current offer levels stable with potential to soften further on possible discounts from producers ahead of the spring season.

PHOSPHATES

Domestic: NOLA DAP was assessed at $545/t FOB to end last month, higher from the previous range at the end of October at $525-$530/t FOB. MAP was assessed $590-$600/t FOB, including domestic sales at the high as well as a lower $590/t FOB reported to have traded on prompt, import product, lower compared to $635-$650/t FOB at the end of October.

River terminal prices began to consolidate in November, ending in a range of $590-$595/t FOB DAP and $670-$680/t FOB MAP. This is compared to October prices of $590-$640/t DAP and $695-$755/t MAP. The main motivator for the erosion of MAP prices at terminals was due to lower demand compared to DAP because of the former's large premium.

Following the Department of Commerce decision to reduce the countervailing duty rate on OCP from 19.97% to just 2.12% in October, Moroccan product has so far not returned in force to the U.S. market. Sources familiar with the trade case expect that Moroccan imports will not surge back into the U.S. market until related legal decisions are fully settled in the international courts, and latest customs figures to date support that assertion.

Phosphate prices are expected to remain mostly stable in the meantime, heading into 2024.

International: The fundamentals of the phosphate market were little changed toward the end of November, characterized by tight supply and with the tone of the market remaining firm. Suppliers were seeking higher prices for phosphates with the tight market and the prospect of healthy demand on the horizon. DAP prices were trending higher in European markets, for example, on good demand relative to tight supply.

In Brazil, this price environment supported a slight increase despite low demand, offset by equally tight supply. Landed prices in the country ended November at $560-$565/mt CFR, up from the $550/mt CFR assessment at the end of October. Meanwhile, prices for DAP in India were maintained across November at $594/mt CFR toward the end of the month, in line with October prices from the month.

The tight supply scenario in the global market was expected to continue into early 2021 with several sellers having already committed sales into January.

POTASH

NOLA granular MOP barges were assessed from $335-$340/t FOB at the end of November, lower from the last weekly assessment of October at $345/t. Most buying activity continued to focus on the terminal and warehouse level for prompt demand for fall applications, while winter fill buying was also informally beginning ahead of expected sales programs from North American producers.

Click here to see more...