By Elliott Dennis

Why the US Government Provides Subsidized Livestock Insurance?

Federally supported livestock insurance is managed by the Federal Crop Insurance Corporation (FCIC) and USDA’s Risk Management Agency (RMA) as part of the Federal crop insurance program. Since 2003, several products are offered for cattle (fed and feeder), swine, dairy, and lamb. Three products developed for cattle producers include livestock risk protection (LRP) for feeder and fed cattle and livestock gross margin (LGM) for fed cattle. LRP seeks to cover losses/decreases in output price. LGM works to cover the decrease in margin between input prices (feeder + corn) and output prices (fed cattle).

Adoption/Use of Livestock Insurance Nationally and in Nebraska

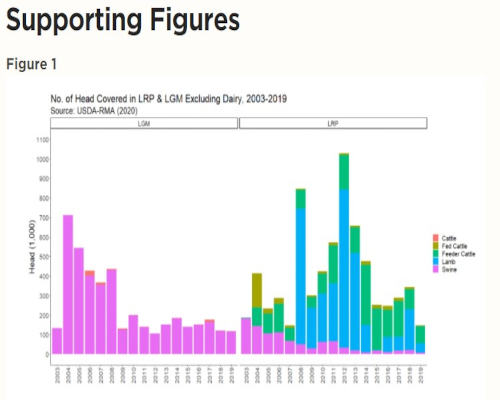

Nationally the use of either LRP or LGM for cattle has been limited (see Figure 1). LGM use is heavily dominated by swine producers. Comparatively the use of federal insurance by cattle is minimal. LRP use is heavily dominated by dairy and lamb. The share of LRP use for swine was relatively large when first introduced in 2003 but has since decreased significantly. LRP fed cattle use is small but stable through time and LRP feeder cattle is larger and stable through time. The overall use of federally provided livestock insurance is still relatively low compared to the total US inventory. Between 2003-2019, 0.13% of total cattle inventory was covered using LGM or LRP. The average of other commodities, except for lamb, are all likewise very low.

Nebraska is the largest user of LRP. Since 2003 approximately 30% of all LRP policies sold were to Nebraska producers. Kansas, South Dakota, and North Dakota are other states that have a historically large share of LRP use. Combined these four states account for 75% of all LRP policies sold in the US. So, while LRP is offered in every US state, the usage of it varies dramatically by region. There are significantly fewer LGM policies sold each year. For example, in 2019 there were 16 policies sold nationwide. Most policies are sold to cattle producers in the Northern Plains. Since 2003 approximately 30% of all LRP policies sold were to Nebraska producers. Iowa, Nebraska, Wisconsin, and North Dakota account for 85% of all LGM policies sold in the US.

Significant Changes to the Livestock Risk Protection (LRP) Insurance Product

The adoption/use of these products is not widespread. One of the primary barriers to use is policy premiums. The government provides subsidies to help producers offset these costs. These subsidy levels have changed dramatically in the last 2 years to make products more affordable compared to other traditional public risk management tools. For example, for LRP, subsidy levels were 13% of premium costs from 2003-2018, 20-35% from 2018 to May 2020, 25-45% from May 2020 to September 2020, and since September 2020 are 35-55%. The subsidy level varies given the percent of ending price one wishes to cover, commonly referred to as the coverage price. Coverage levels vary from 70-100% of the ending price.

In addition to the changes in subsidy levels, there have been several other changes that should significantly increase the use of LRP. These include increasing head limits to 6,000 head per endorsement/12,000 head annually for fed and feeder cattle, modifying the livestock ownership requirement to 60 days and allowing the purchase of insurance before physical ownership (i.e. calving), removing the A&O cap of $20 million, and allowing producers to pay the premium after the endorsement period has ended. All of these remove barriers that have historically prohibited the use of LRP. One barrier that remains in place, and unlikely to ever be removed, is that LRP must be purchased after CME trading hours (i.e. 4 pm-10 am EDT). To find crop insurance agents in your area that are currently qualified to sell LRP can be found here.

Differences and Similarities of LRP and CME Options

One of the primary objectives of LRP is to provide a cost-effective risk management product to the producer. The contract size is a significant barrier to producer CME futures and options use. One benefit of the LRP insurance product is that it allows a flexible amount of coverage based on total production weight.

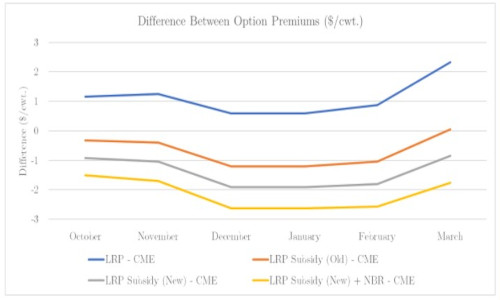

LRP premiums being too expensive is a common comment made by cattle producers. Comparing premium costs to CME options is one way to measure how expensive, if at all, LRP premiums are. If LRP insurance premiums are cheaper relative to CME options, then a profit-maximizing producer would shift risk management from CME options to LRP. The opposite is also true. Figure 2 plots the premium cost differential between LRP insurance and CME options both with and without subsidy levels. Positive numbers imply that for a given endorsement length, LRP is relatively more expensive than a CME option. Negative values imply LRP is relatively cheaper than a CME option. Further, it shows that the newly established subsidy levels, make LRP considerably cheaper than CME options. Given current and potential future market disruptions, using LRP is one tool that can be affordable for producers to manage output price risk.

Source : unl.edu